The Fund will invest in exchange traded funds (ETFs) listed for trading on US exchanges selected by the Manager using a systematic algorithmic approach, referred to as the Adaptive Asset Allocation™ process. This approach rotates investment holdings into a selection of the strongest performing global assets or the most defensive assets in any given market condition. This process of continuous asset performance and selection allows the Fund’s investment holdings to adapt to changing markets and risk environments.

The Adaptive Asset Allocation™ process also provides a strong framework for risk management, mainly by requiring regular re-assessment of existing holdings as against other holdings and potential new investments.

Analysis of this strategy shows outperformance against the benchmark of the S&P 500 index since 2003 with significantly less volatility and markedly lower equity drawdowns. When back-tested throughout the period of the global financial crisis 2007–2009, the application of the Adaptive Asset Allocation™ process simulated for the Fund was profitable. Of course, back testing and any past performance is no assurance of actual future performance of the Fund, since market conditions can change, assumptions may be wrong and there are differences between direct trading and investing via a managed fund (e.g., different costs), but back testing under those conditions remains valid and highly relevant and is a significant indictor that should be taken into account.

In most market conditions, there are typically assets that perform well, whether that is a strong market rally in the US or an industry segment in that market, a gold rally, interest rate trends, alternative assets, emerging markets, bonds or even cash. The Fund through its disciplined Adaptive Asset Allocation™ process will typically be invested in a basket of ETFs that are performing the strongest in the short to mid-term and thus capturing mid- term momentum effects whilst factoring in asset volatility and absolute asset performance. Momentum is a core element in the Fund’s Adaptive Asset Allocation™ Process.

The momentum effect in asset class performance across asset classes has been well researched and documented over many years (Jegadeesh and Titman (1993), Asness (1994), Moskowitz and Pederson (2012)). The tendency of assets that have done well over a 6-12 month period to continue to perform has been referred to as one of the strongest and most pervasive phenomena in financial markets (Antonacci (2012)). Indeed momentum has been described as “… the premier market anomaly” by academics (Fama and French (2008)).

Momentum has been shown to work both on a relative basis, that is, in which an asset’s performance relative to other assets predicts its future relative performance, and also on an absolute basis, that is, an asset’s own past performance measured against its own past performance as an indicator of future performance (Moskowitz, Ooi and Pederson (2012)). Absolute momentum has been shown to be as relevant across multiple asset classes going back to the turn of the 20th Century (Hurst, Ooi and Pedersen (2012)).

The combination of these principles and other factors such as volatility, asset diversification and risk management are incorporated into the Fund‘s Adaptive Asset Allocation™ process, which uses ETFs to provide exposure to a wide range of global assets.

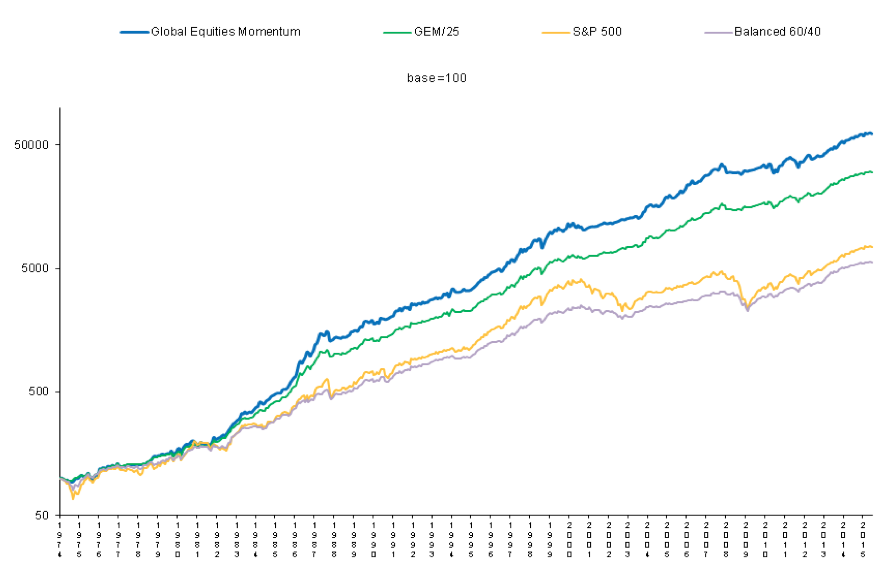

An example of the application of a Dual momentum model ‘GEM’ an approach popularised by Gary Antonacci.

In an article on Seeking Alpha he summarises the process as; ‘GEM‘s core holding is the S&P 500 index in order to capture the highest long-run risk premium. GEM switches between U.S. and international stocks according to relative strength price momentum, which can improve the expected return from holding stocks. The GEM model also switches between stocks and bonds in accordance with trend-following absolute (time-series) momentum. When equities have been going up according to the rules of absolute momentum, GEM stays fully invested in stocks. When the trend of the stock market turns negative, GEM switches into low-duration aggregate bonds.

The graph below compares the returns of the GEM approach vs the SP500 and a more traditional asset allocation of 60 Equities / 40 % Bonds. It is also shows the result of allocating 75% to GEM and 25% to Bonds.

Gary Antonacci July 21 2015

http://seekingalpha.com/article/3341645-back-to-fundamentals

Returns: GEM 17.73% p.a. GEM/25 15.35% p.a. S&P 500 index 12.33% p.a. Balanced 60/40 10.76% p.a.

Research and further reading related to Momentum is available in the research section of this website.

US listed ETFs provide access to an extensive array of global assets. ETFs can provide investment exposure to a wide range of asset classes, countries, regions, commodities, bonds, FX, inverse market exposure and alternate assets. There were 1577 US listed ETFs with assets under management of USD2.878 trillion as at end 2015.

The investment strategy for the Fund selects ETFs from a universe of those with a market capitalisation in excess of USD400million and demonstrating strong daily market liquidity.

Investment selection for the Fund is made from a universe of over 50 ETFs which are divided initially into four baskets or categories. The number and composition of baskets may be changed in the future at the discretion of the Manager.

The four initial ETF baskets provide portfolio diversification and in combination exhibit a less than 0.50 correlation with the S&P 500 index in a back-test of the Adaptive Asset Allocation™ process between February 2003 and July 2016.

The four initial EFT baskets are:

A strictly algorithmic approach is taken to the ETF performance evaluation and investment selection. First, absolute relative strength is evaluated – only ETFs in each basket that have outperformed the US cash rate or against their 6 month moving average are considered for selection. If none of the ETFs exceed the thresholds assigned to each basket then the investment selection will revert to cash. A cash investment is made through purchase of the US listed short term 2 year US treasury bonds ETF (SHY).

Of the remaining selected ETFs, the top performing ETF from each of the four baskets is selected for investment based on a calculation of performance over multiple timeframes and volatility factors. The timeframe is typically a weighted period of two time periods varying from 2 to 6 months. In addition, the volatility of each ETF over a time period is evaluated. High performance of an ETF is positive and high volatility is negative in the relative ranking process of the universe of each ETF basket.

Other than at rare times of extreme market stress where the Fund may be defensively positioned in cash, the Fund will typically hold four ETFs, one from each basket. The four baskets are equally weighted with 25% in each basket.

The investment selection is reviewed. Assets are adjusted if required and rebalanced twice monthly or monthly (basket reset timing varies). The ETF which ranks the highest in each basket continues to be held until they no longer hold that ranking, and they are replaced by the new top performer. Thus the assets being held are the highest performers against the selection criteria.

Further details are provided in the Documents Section of this website. A summary of the key features of the SIML Global ETF Fund and summary details in a Q&A format are outlined below. These should be read in conjunction with the full Information Memorandum.